Hong Kong Student Housing: Saturated After the Recent Deal Spree?

- Raymond Choi

- May 7

- 4 min read

Since August 2025, the Hong Kong student housing sector has been brewing beneath the surface of weak real estate sentiment following Covid and the rise of interest rates from 2022. In less than nine months as of April 2026, nine en-bloc hotel or residential properties totaling HK$4.626 billion (USD 590 million) consisting of 3,200 beds have transacted by private or global real estate investment funds, universities, as well as developers. I have been asked many times in recent months whether the Hong Kong student housing market may be saturated with the large surge in supply. This article serves to answer this key question based on latest market data.

Demand: Non-local students to rise 28% by 2029/30

The key driver in the rise of non-local student population beginning from the 2024/25 school year was the government's initiative to increase the admission quote of non-local students from 20% to 40%. This was further increased to 50% in the 2025 Policy Address with the aim to enhance the city's appeal as an international education hub.

Based on the latest published non-local student and total university enrollment statistics for 2024/25, for UGC non-local students to achieve the government's target quota of 50%, non-local students will need to rise from the current 92,000 to 118,200 by 2029/30. In the analysis, I have conservatively assumed that it will take 5 years for universities to ramp up school infrastructure and courses in preparation for this incremental 26,200 student intake.

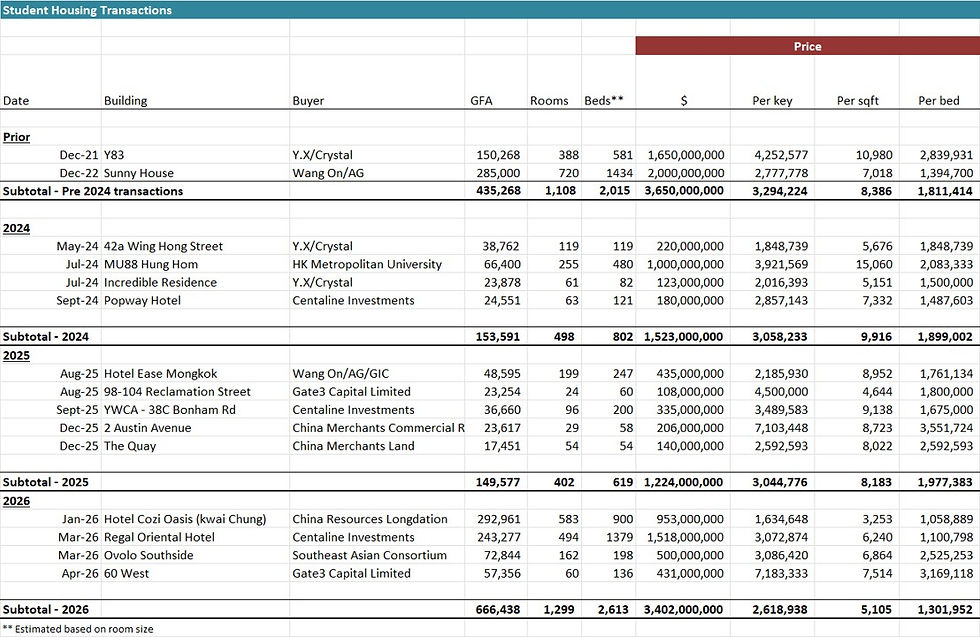

Detailed student beds supply breakdown

The below is a detailed breakdown of all private student housing transactions in recent years:

From the above table, the momentum of residential or hotel property transactions, being a value-add conversion play into student housing, really picked up since August 2025 after the one-month HIBOR dropped from around 4% to as low as below 1%. The HIBOR has since rebounded to approximately 2% to 2.5% but this was sufficient to kick start acquisitions in this sector.

Private Sector

Since August 2025, HK $4.6 billion worth of transactions across 9 en-bloc residential or hotel properties have taken place, translating into 1,700 rooms and 3,232 student beds in the private sector from acquisitions. Centaline Investments, one of the two largest operators in the city, recently announced that they will increase their target student beds from 2,000 to 6,000 over the next few years. From the above table, the company currently has 1,700 student beds under management.

From development perspective, there are two notable projects in the pipeline. One is the recently announced pre-commitment by The Hang Seng University to take student spaces at the 18 Ting Yip Street development project in Ngau Tau Kok, a joint venture between Wang On Properties and APG Asset Management. This will add another 300 beds by the 2027/2028 school year. Another notable development is by Star Properties located at 103-109 Wai Yip Street in Kwun Tong which is expected to add another 1,300 student beds to the pipeline. In total, private developments will add an additional 1,600 beds over the next 2 to 3 years.

In totality, the private sector will likely see an increase of 9,132 beds based on all announced acquisitions and developments. This figure includes the assumption that Centaline Investment will meet the target 6,000 beds in three years.

University & Public Sector Supply

Based on all publicly available disclosures and university announcements, I have compiled the following summary of announced student housing projects over the next three years:

City University of Hong Kong: 3,493 beds

Chinese University of Hong Kong: 850 beds

University of Hong Kong: 938 beds

The Hong Kong Polytechnic University: 2,959 beds

Metropolitan University: 430 beds

In totality, total university supply equates to 8,670 student beds.

The Hong Kong government has also announced the following initiatives in the past year:

The government now allows the conversion of offices and hotels into student housing without lease modification and land premium. The government has received 25 cases involving 5,100 beds, 23 of which most will be in the form of modification of existing property, while two are development projects.

Government land tender specifically for student housing: In Q1 2026, the government has sent invitation for Expressions of Interests (EOI) for three commercial sites (Kai Tak, Shatin & Tung Chung East) to provide 4,500 beds. It is reported in March that 22 EOIs were received. However, it is expected the completion of these sites will likely be in 2029/2030 at the earliest.

In totality, total potential supply over the next 4 years from government initiatives is 9,600 student beds.

Putting all the numbers together

Based on all market data above, the expected student beds shortage is expected to rise from 48,881 in the 2024/25 school year to approximately 55,000 by 2029. This shortfall represents 13.6x beds created (4,034 beds) from all private en-bloc transactions since early 2024. This implies that the combined supply from private en-bloc residential and hotel properties sold in the past year, university hostel projects, and government initiatives can only partially offset the rise in student intake from increasing the non-local student quote to 50%. It is unlikely to be able to address existing shortage in this space.

In summary, the student housing market is unlikely to be saturated from a supply perspective in the medium term. A more imminent bottleneck for private investors is the availability of properties suitable for conversion into student housing and the number of qualified operators available to run the strategy for institutional LPs.

Comments